sur Delticom AG (ETR:DEX)

Delticom AG Maintains BUY Rating Amid Strategic Shift

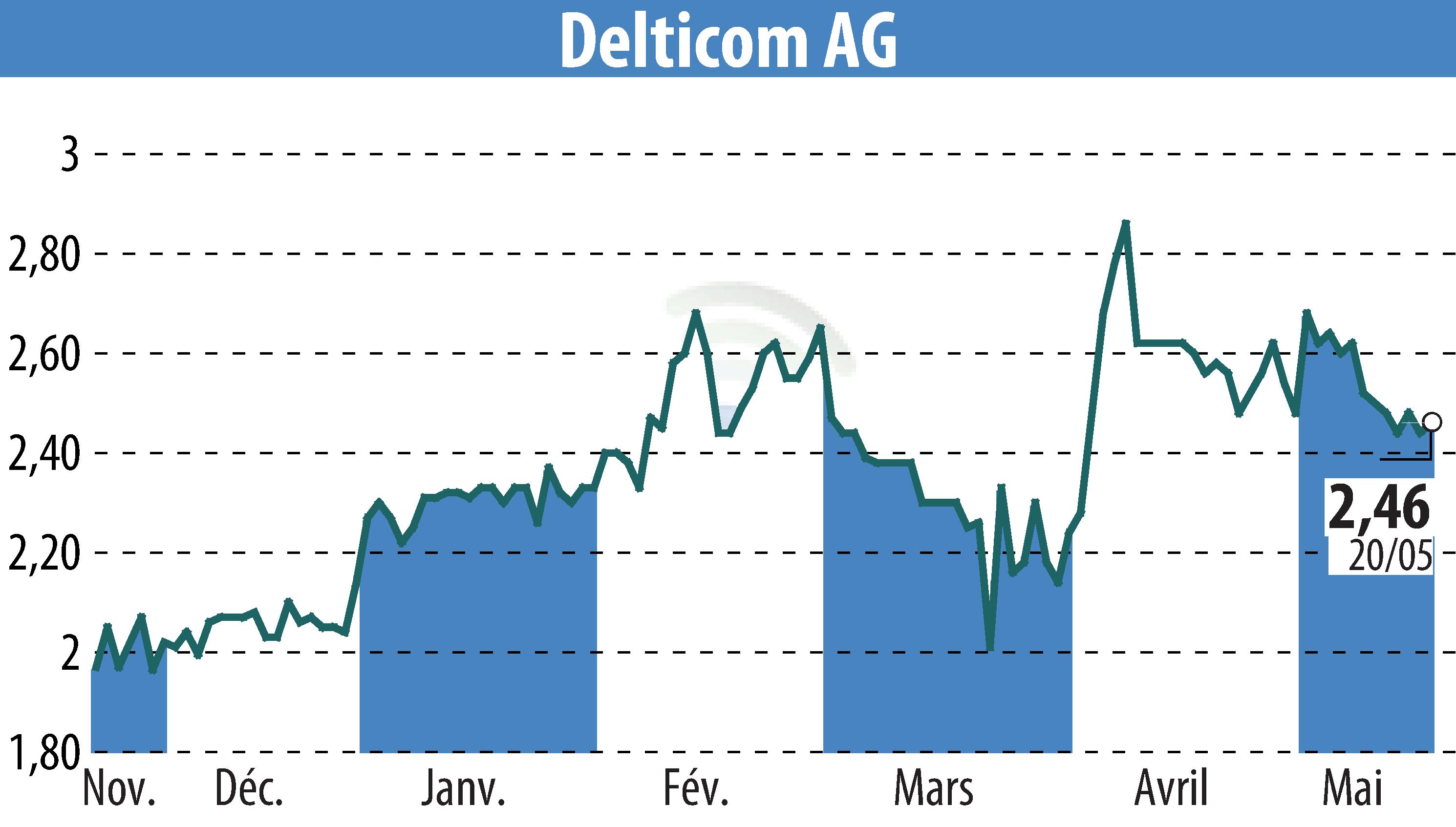

Delticom AG's latest update reveals a strategic shift from growth-driven to margin-focused operations. Quirin Privatbank Kapitalmarktgeschäft continues to recommend buying, despite a year-on-year revenue drop of 6.1%. The first quarter saw a net result of EUR -1.2m, matching last year's figures, while operating EBITDA reached EUR 1.1m.

The company's reaffirmed full-year guidance indicates expected revenues between EUR 480-520m and operating EBITDA of EUR 19-24m. The upcoming quarters, traditionally stronger for tire sales, are anticipated to boost profitability.

Factors such as the seasonal demand for summer and winter tires, lower fixed costs post-DeltiLog deconsolidation, and an increased mix of high-margin all-season tires support this outlook. However, due to macroeconomic challenges, projections are conservatively positioned at the lower end.

R. E.

Copyright © 2026 FinanzWire, tous droits de reproduction et de représentation réservés.

Clause de non responsabilité : bien que puisées aux meilleures sources, les informations et analyses diffusées par FinanzWire sont fournies à titre indicatif et ne constituent en aucune manière une incitation à prendre position sur les marchés financiers.

Cliquez ici pour consulter le communiqué de presse ayant servi de base à la rédaction de cette brève

Voir toutes les actualités de Delticom AG